Bayesian Estimation and Forecasting of Time Series in statsmodels

Abstract¶

Statsmodels, a Python library for statistical and econometric analysis,

has traditionally focused on frequentist inference, including in its

models for time series data. This paper introduces the powerful features

for Bayesian inference of time series models that exist in statsmodels, with

applications to model fitting, forecasting, time series decomposition,

data simulation, and impulse response functions.

Introduction¶

Statsmodels Seabold & Perktold, 2010 is a well-established Python

library for statistical and econometric analysis, with support for a wide range

of important model classes, including linear regression, ANOVA, generalized

linear models (GLM), generalized additive models (GAM), mixed effects models,

and time series models, among many others. In most cases, model fitting proceeds

by using frequentist inference, such as maximum likelihood estimation (MLE). In

this paper, we focus on the class of time series models

McKinney et al., 2011, support for which has grown substantially in

statsmodels over the last decade. After introducing several of the most

important new model classes – which are by default fitted using MLE – and

their features – which include forecasting, time series decomposition and

seasonal adjustment, data simulation, and impulse response analysis – we

describe the powerful functions that enable users to apply Bayesian methods to

a wide range of time series models.

Support for Bayesian inference in Python outside of statsmodels has also grown

tremendously, particularly in the realm of probabilistic programming, and

includes powerful libraries such as

PyMC3 Salvatier et al., 2016, PyStan Carpenter et al., 2017,

and TensorFlow Probability Dillon et al., 2017. Meanwhile,

ArviZ Kumar et al., 2019 provides many excellent tools for associated

diagnostics and vizualisations. The aim of these libraries is to provide support

for Bayesian analysis of a large class of models, and they make available both

advanced techniques, including auto-tuning algorithms, and flexible model

specification. By contrast, here we focus on simpler techniques. However, while

the libraries above do include some support for time series models, this has not

been their primary focus. As a result, introducing Bayesian inference for the

well-developed stable of time series models in statsmodels, and providing

access to the rich associated feature set already mentioned, presents a

complementary option to these more general-purpose libraries.[1]

Time series analysis in statsmodels¶

A time series is a sequence of observations ordered in time, and time series data appear commonly in statistics, economics, finance, climate science, control systems, and signal processing, among many other fields. One distinguishing characteristic of many time series is that observations that are close in time tend to be more correlated, a feature known as autocorrelation. While successful analyses of time series data must account for this, statistical models can harness it to decompose a time series into trend, seasonal, and cyclical components, produce forecasts of future data, and study the propagation of shocks over time.

We now briefly review the models for time series data that are available in

statsmodels and describe their features.[2]

Exponential smoothing models¶

Exponential smoothing models are constructed by combining one or more simple equations that each describe some aspect of the evolution of univariate time series data. While originally somewhat ad hoc, these models can be defined in terms of a proper statistical model (for example, see Hyndman et al. (2008)). They have enjoyed considerable popularity in forecasting (for example, see the implementation in R described by Hyndman & Athanasopoulos (2018)). A prototypical example that allows for trending data and a seasonal component – often known as the additive “Holt-Winters’ method” – can be written as

where is the level of the series, is the trend,

is the seasonal component of period , and

are parameters of the model. When augmented with

an error term with some given probability distribution (usually Gaussian),

likelihood-based inference can be used to estimate the parameters.

In statsmodels, additive exponential smoothing models

can be constructed using the statespace.ExponentialSmoothing class.[3]

The following code shows how to apply the additive Holt-Winters model above to

model quarterly data on consumer prices:

import statsmodels.api as sm

# Load data

mdata = sm.datasets.macrodata.load().data

# Compute annualized consumer price inflation

y = np.log(mdata['cpi']).diff().iloc[1:] * 400

# Construct the Holt-Winters model

model_hw = sm.tsa.statespace.ExponentialSmoothing(

y, trend=True, seasonal=12)Structural time series models¶

Structural time series models, introduced by Harvey (1990) and also sometimes known as unobserved components models, similarly decompose a univariate time series into trend, seasonal, cyclical, and irregular components:

where is the trend, is the seasonal component,

is the cyclical component, and

is the error term. However, this

equation can be augmented in many ways, for example to include explanatory

variables or an autoregressive component. In addition, there are many possible

specifications for the trend, seasonal, and cyclical components, so that a wide

variety of time series characteristics can be accommodated. In statsmodels,

these models can be constructed from the UnobservedComponents class; a

few examples are given in the following code:

# "Local level" model

model_ll = sm.tsa.UnobservedComponents(y, 'llevel')

# "Local linear trend", with seasonal component

model_arma11 = sm.tsa.UnobservedComponents(

y, 'lltrend', seasonal=4)These models have become popular for time series analysis and forecasting, as they are flexible and the estimated components are intuitive. Indeed, Google’s Causal Impact library Brodersen et al., 2015 uses a Bayesian structural time series approach directly, and Facebook’s Prophet library Taylor & Letham, 2017 uses a conceptually similar framework and is estimated using PyStan.

Autoregressive moving-average models¶

Autoregressive moving-average (ARMA) models, ubiquitous in time series

applications, are well-supported in statsmodels, including their

generalizations, abbreviated as “SARIMAX”, that allow for integrated time series

data, explanatory variables, and seasonal effects.[4] A general version of

this model, excluding integration, can be written as

where . These are constructed in

statsmodels with the ARIMA class; the following code shows how to

construct a variety of autoregressive moving-average models for consumer price

data:

# AR(2) model

model_ar2 = sm.tsa.ARIMA(y, order=(2, 0, 0))

# ARMA(1, 1) model with explanatory variable

X = mdata['realint']

model_arma11 = sm.tsa.ARIMA(

y, order=(1, 0, 1), exog=X)

# SARIMAX(p, d, q)x(P, D, Q, s) model

model_sarimax = sm.tsa.ARIMA(

y, order=(p, d, q), seasonal_order=(P, D, Q, s))While this class of models often produces highly competitive forecasts, it does not produce a decomposition of a time series into, for example, trend and seasonal components.

Vector autoregressive models¶

While the SARIMAX models above handle univariate series, statsmodels also has

support for the multivariate generalization to vector autoregressive (VAR)

models.[5] These models are written

where is now considered as an vector. As a result,

the intercept ν is also an vector, the

coefficients are each matrices, and the error

term is , with Ω an

matrix. These models can be constructed in statsmodels

using the VARMAX class, as follows[6]

# Multivariate dataset

z = (np.log(mdata['realgdp', 'realcons', 'cpi'])

.diff().iloc[1:])

# VAR(1) model

model_var = sm.tsa.VARMAX(z, order=(1, 0))Dynamic factor models¶

statsmodels also supports a second model for multivariate time series: the

dynamic factor model (DFM). These models, often used for dimension reduction,

posit a few unobserved factors, with autoregressive dynamics, that are used to

explain the variation in the observed dataset. In statsmodels, there are two

model classes, DynamicFactor and DynamicFactorMQ, that can fit

versions of the DFM. Here we focus on the DynamicFactor class, for which

the model can be written

Here again, the observation is assumed to be , but the factors are , where it is possible that . As before, we assume conformable coefficient matrices and Gaussian errors.

The following code shows how to construct a DFM in statsmodels

# DFM with 2 factors that evolve as a VAR(3)

model_dfm = sm.tsa.DynamicFactor(

z, k_factors=2, factor_order=3)Linear Gaussian state space models¶

Figure 1:Selected functionality of state space models in statsmodels.

In statsmodels, each of the model classes introduced above (

statespace.ExponentialSmoothing, UnobservedComponents,

ARIMA, VARMAX, DynamicFactor, and

DynamicFactorMQ) are implemented as part of a broader class of models,

referred to as linear Gaussian state space models (hereafter for brevity, simply

“state space models” or SSM). This class of models can be written as

where represents an unobserved vector containing the “state” of the dynamic system. In general, the model is multivariate, with and vector, , and .

Powerful tools exist for state space models to estimate the

values of the unobserved state vector, compute the value of the likelihood

function for frequentist inference, and perform posterior sampling for Bayesian

inference. These tools include the celebrated Kalman filter and smoother and

a simulation smoother, all of which are important for conducting Bayesian

inference for these models.[7] The implementation in statsmodels largely follows

the treatment in Durbin & Koopman (2012), and is described in more detail in

Fulton (2015).

In addition to these key tools, state space models also admit general implementations of useful features such as forecasting, data simulation, time series decomposition, and impulse response analysis. As a consequence, each of these features extends to each of the time series models described above. Figure 1 presents a diagram showing how to produce these features, and the code below briefly introduces a subset of them.

# Construct the Model

model_ll = sm.tsa.UnobservedComponents(y, 'llevel')

# Construct a simulation smoother

sim_ll = model_ll.simulation_smoother()

# Parameter values (variance of error and

# variance of level innovation, respectively)

params = [4, 0.75]

# Compute the log-likelihood of these parameters

llf = model_ll.loglike(params)

# `smooth` applies the Kalman filter and smoother

# with a given set of parameters and returns a

# Results object

results_ll = model_ll.smooth(params)

# Produce forecasts for the next 4 periods

fcast = results_ll.forecast(4)

# Produce a draw from the posterior distribution

# of the state vector

sim_ll.simulate()

draw = sim_ll.simulated_stateNearly identical code could be used for any of the model classes introduced above, since they are all implemented as part of the same state space model framework. In the next section, we show how these features can be used to perform Bayesian inference with these models.

Bayesian inference via Markov chain Monte Carlo¶

We begin by giving a cursory overview of the key elements of Bayesian inference required for our purposes here.[8] In brief, the Bayesian approach stems from Bayes’ theorem, in which the posterior distribution for an object of interest is derived as proportional to the combination of a prior distribution and the likelihood function

Here, we will be interested in the posterior distribution of the parameters

of our model and of the unobserved states, conditional on the chosen model

specification and the observed time series data. While in most cases the form

of the posterior cannot be derived analytically, simulation-based methods such

as Markov chain Monte Carlo (MCMC) can be used to draw samples that approximate

the posterior distribution nonetheless. While PyMC3, PyStan, and TensorFlow

Probability emphasize Hamiltonian Monte Carlo (HMC) and no-U-turn sampling

(NUTS) MCMC methods, we focus on the simpler random walk Metropolis-Hastings

(MH) and Gibbs sampling (GS) methods. These are standard MCMC methods that

have enjoyed great success in time series applications and which are simple to

implement, given the state space framework already available in statsmodels.

In addition, the ArviZ library is designed to work with MCMC output from any

source, and we can easily adapt it to our use.

With either Metropolis-Hastings or Gibbs sampling, our procedure will produce a sequence of sample values (of parameters and / or the unobserved state vector) that approximate draws from the posterior distribution arbitrarily well, as the number of length of the chain of samples becomes very large.

Random walk Metropolis-Hastings¶

In random walk Metropolis-Hastings (MH), we begin with an arbitrary point as the initial sample, and then iteratively construct new samples in the chain as follows. At each iteration, (a) construct a proposal by perturbing the previous sample by a Gaussian random variable, and then (b) accept the proposal with some probability. If a proposal is accepted, it becomes the next sample in the chain, while if it is rejected then the previous sample value is carried over. Here, we show how to implement Metropolis-Hastings estimation of the variance parameter in a simple model, which only requires the use of the log-likelihood computation introduced above.

import arviz as az

from scipy import stats

# Construct the model

model_rw = sm.tsa.UnobservedComponents(y, 'rwalk')

# Specify the prior distribution. With MH, this

# can be freely chosen by the user

prior = stats.uniform(0.0001, 100)

# Specify the Gaussian perturbation distribution

perturb = stats.norm(scale=0.1)

# Storage

niter = 100000

samples_rw = np.zeros(niter + 1)

# Initialization

samples_rw[0] = y.diff().var()

llf = model_rw.loglike(samples_rw[0])

prior_llf = prior.logpdf(samples_rw[0])

# Iterations

for i in range(1, niter + 1):

# Compute the proposal value

proposal = samples_rw[i - 1] + perturb.rvs()

# Compute the acceptance probability

proposal_llf = model_rw.loglike(proposal)

proposal_prior_llf = prior.logpdf(proposal)

accept_prob = np.exp(

proposal_llf - llf

+ prior_llf - proposal_prior_llf)

# Accept or reject the value

if accept_prob > stats.uniform.rvs():

samples_rw[i] = proposal

llf = proposal_llf

prior_llf = proposal_prior_llf

else:

samples_rw[i] = samples_rw[i - 1]

# Convert for use with ArviZ and plot posterior

samples_rw = az.convert_to_inference_data(

samples_rw)

# Eliminate the first 10000 samples as burn-in;

# thin by factor of 10 to reduce autocorrelation

az.plot_posterior(samples_rw.posterior.sel(

{'draw': np.s_[10000::10]}), kind='bin',

point_estimate='median')

Figure 2:Approximate posterior distribution of variance parameter, random walk model, Metropolis-Hastings; U.S. Industrial Production.

The approximate posterior distribution, constructed from the sample chain, is shown in Figure 2.

Gibbs sampling¶

Gibbs sampling (GS) is a special case of Metropolis-Hastings (MH) that is applicable when it is possible to produce draws directly from the conditional distributions of every variable, even though it is still not possible to derive the general form of the joint posterior. While this approach can be superior to random walk MH when it is applicable, the ability to derive the conditional distributions typically requires the use of a “conjugate” prior – i.e., a prior from some specific family of distributions. For example, above we specified a uniform distribution as the prior when sampling via MH, but that is not possible with Gibbs sampling. Here, we show how to implement Gibbs sampling estimation of the variance parameter, now making use of an inverse Gamma prior, and the simulation smoother introduced above.

Figure 3:Approximate posterior joint distribution of variance parameters, local level model, Gibbs sampling; CPI inflation.

# Construct the model and simulation smoother

model_ll = sm.tsa.UnobservedComponents(y, 'llevel')

sim_ll = model_ll.simulation_smoother()

# Specify the prior distributions. With GS, we must

# choose an inverse Gamma prior for each variance

priors = [stats.invgamma(0.01, scale=0.01)] * 2

# Storage

niter = 100000

samples_ll = np.zeros((niter + 1, 2))

# Initialization

samples_ll[0] = [y.diff().var(), 1e-5]

# Iterations

for i in range(1, niter + 1):

# (a) Update the model parameters

model_ll.update(samples_ll[i - 1])

# (b) Draw from the conditional posterior of

# the state vector

sim_ll.simulate()

sample_state = sim_ll.simulated_state.T

# (c) Compute / draw from conditional posterior

# of the parameters:

# ...observation error variance

resid = y - sample_state[:, 0]

post_shape = len(resid) / 2 + 0.01

post_scale = np.sum(resid**2) / 2 + 0.01

samples_ll[i, 0] = stats.invgamma(

post_shape, scale=post_scale).rvs()

# ...level error variance

resid = sample_state[1:] - sample_state[:-1]

post_shape = len(resid) / 2 + 0.01

post_scale = np.sum(resid**2) / 2 + 0.01

samples_ll[i, 1] = stats.invgamma(

post_shape, scale=post_scale).rvs()

# Convert for use with ArviZ and plot posterior

samples_ll = az.convert_to_inference_data(

{'parameters': samples_ll[None, ...]},

coords={'parameter': model_ll.param_names},

dims={'parameters': ['parameter']})

az.plot_pair(samples_ll.posterior.sel(

{'draw': np.s_[10000::10]}), kind='hexbin');The approximate posterior distribution, constructed from the sample chain, is shown in Figure 3.

Illustrative examples¶

For clarity and brevity, the examples in the previous section gave results for simple cases. However, these basic methods carry through to each of the models introduced earlier, including in cases with multivariate data and hundreds of parameters. Moreover, the Metropolis-Hastings approach can be combined with the Gibbs sampling approach, so that if the end user wishes to use Gibbs sampling for some parameters, they are not restricted to choose only conjugate priors for all parameters.

In addition to sampling the posterior distributions of the parameters, this method allows sampling other objects of interest, including forecasts of observed variables, impulse response functions, and the unobserved state vector. This last possibility is especially useful in cases such as the structural time series model, in which the unobserved states correspond to interpretable elements such as the trend and seasonal components. We provide several illustrative examples of the various types of analysis that are possible.

Forecasting and Time Series Decomposition¶

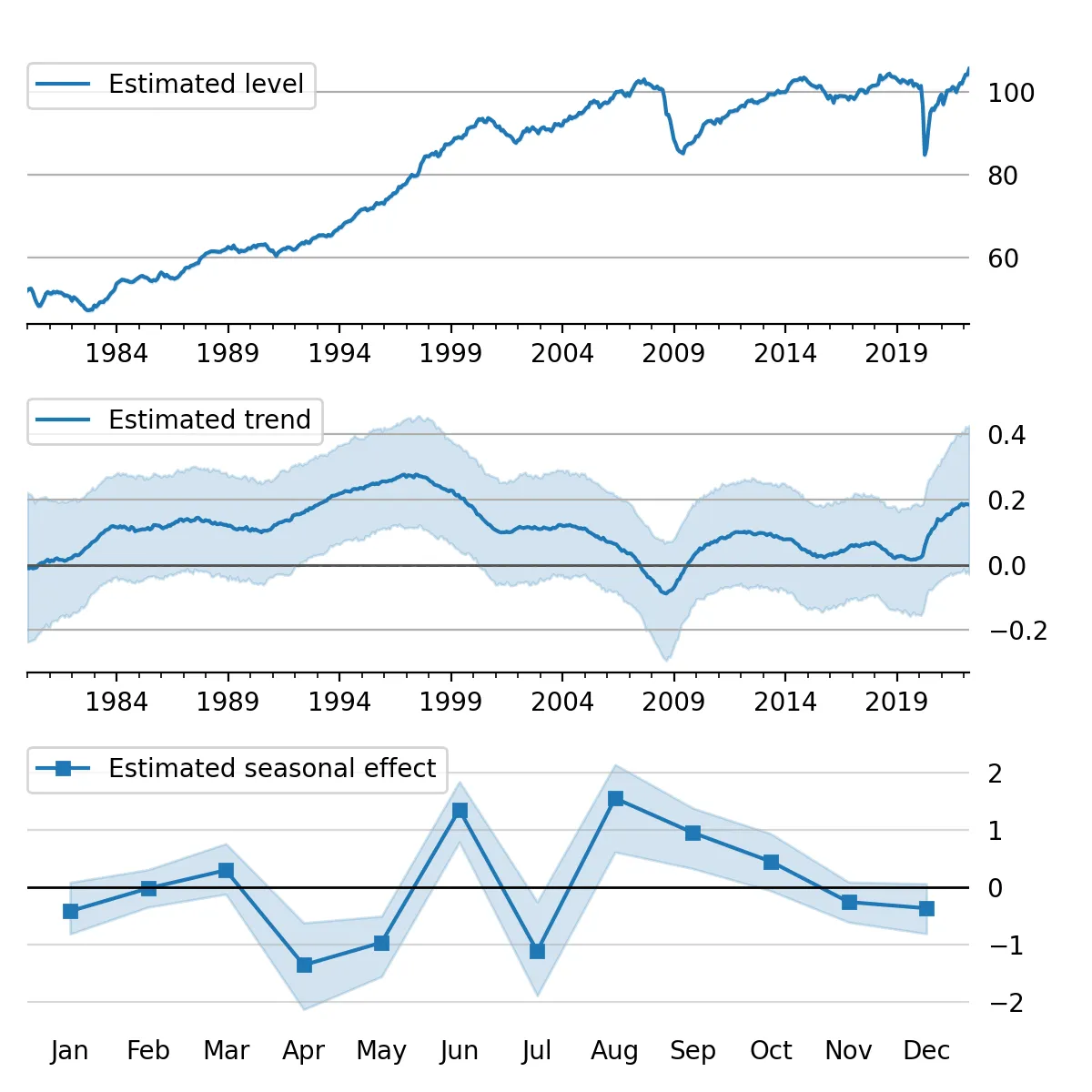

Figure 4:Data and forecast with 80% credible interval; U.S. Industrial Production.

Figure 5:Estimated level, trend, and seasonal components, with 80% credible interval; U.S. Industrial Production.

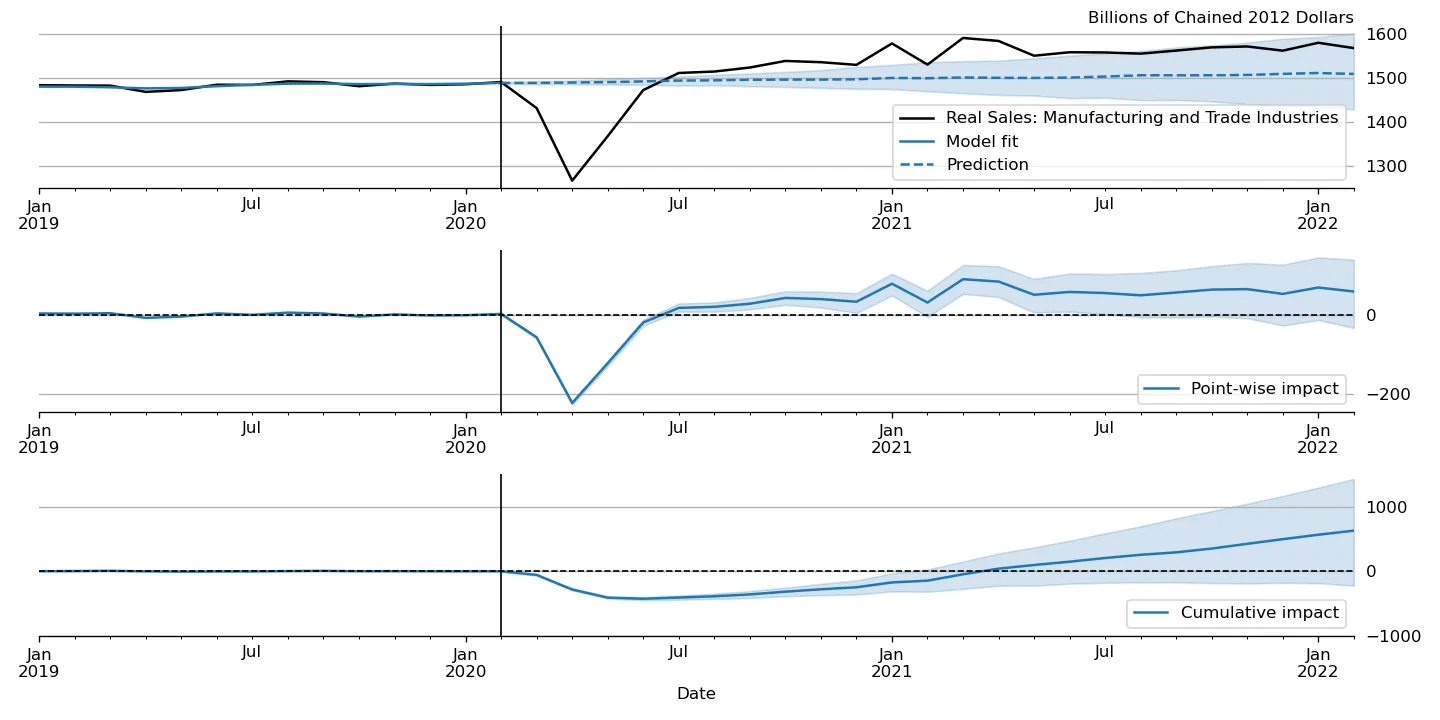

Figure 6:“Causal impact” of COVID-19 on U.S. Sales in Manufacturing and Trade Industries.

In our first example, we apply the Gibbs sampling approach to a structural time series model in order to forecast U.S. Industrial Production and to produce a decomposition of the series into level, trend, and seasonal components. The model is

Here, we set the seasonal periodicity to s=12, since Industrial Production is

a monthly variable. We can construct this model in Statsmodels as[9]

model = sm.tsa.UnobservedComponents(

y, 'lltrend', seasonal=12)To produce the time-series decomposition into level, trend, and seasonal

components, we will use samples from the posterior of the state vector

for each time period . These are

immediately available when using the Gibbs sampling approach; in the earlier

example, the draw at each iteration was assigned to the variable sample_state.

To produce forecasts, we need to draw from the posterior predictive

distribution for horizons . This can

be easily accomplished by using the simulate method introduced earlier. To be

concrete, we can accomplish these tasks by modifying section (b) of our Gibbs

sampler iterations as follows:

# (b') Draw from the conditional posterior of

# the state vector

model.update(params[i - 1])

sim.simulate()

# save the draw for use later in time series

# decomposition

states[i] = sim.simulated_state.T

# Draw from the posterior predictive distribution

# using the `simulate` method

n_fcast = 48

fcast[i] = model.simulate(

params[i - 1], n_fcast,

initial_state=states[i, -1]).to_frame()These forecasts and the decomposition into level, trend, and seasonal components are summarized in Figure 4 and Figure 5, which show the median values along with 80% credible intervals. Notably, the intervals shown incorporate for both the uncertainty arising from the stochastic terms in the model as well as the need to estimate the models’ parameters.[10]

Casual impacts¶

A closely related procedure described in Brodersen et al. (2015) uses a Bayesian structural time series model to estimate the “causal impact” of some event on some observed variable. This approach stops estimation of the model just before the date of an event and produces a forecast by drawing from the posterior predictive density, using the procedure described just above. It then uses the difference between the actual path of the data and the forecast to estimate impact of the event.

An example of this approach is shown in Figure 6, in which we use this method to illustrate the effect of the COVID-19 pandemic on U.S. Sales in Manufacturing and Trade Industries.[11]

Extensions¶

There are many extensions to the time series models presented here that are

made possible when using Bayesian inference. First, it is easy to create custom

state space models within the statsmodels framework. As one example, the

statsmodels documentation describes how to create a model that extends the

typical VAR described above with time-varying parameters.[12] These custom

state space models automatically inherit all the functionality described above,

so that Bayesian inference can be conducted in exactly the same way.

Second, because the general state space model available in statsmodels and

introduced above allows for time-varying system matrices, it is possible using

Gibbs sampling methods to introduce support for automatic outlier handling,

stochastic volatility, and regime switching models, even though these are

largely infeasible in statsmodels when using frequentist methods such as

maximum likelihood estimation.[13]

Conclusion¶

This paper introduces the suite of time series models available in statsmodels

and shows how Bayesian inference using Markov chain Monte Carlo methods can be

applied to estimate their parameters and produce analyses of interest, including

time series decompositions and forecasts.

Copyright © 2022 Fulton. This is an open-access article distributed under the terms of the Creative Commons Attribution 3.0 Unported license.

In addition, it is possible to combine the sampling algorithms of PyMC3 with the time series models of

statsmodels, although we will not discuss this approach in detail here. See, for example, https://www .statsmodels .org /v0 .13 .0 /examples /notebooks /generated /statespace _sarimax _pymc3 .html. In addition to statistical models,

statsmodelsalso provides a number of tools for exploratory data analysis, diagnostics, and hypothesis testing related to time series data; see https://www .statsmodels .org /stable /tsa .html. A second class,

ETSModel, can also be used for both additive and multiplicative models, and can exhibit superior performance with maximum likelihood estimation. However, it lacks some of the features relevant for Bayesian inference discussed in this paper.Note that in

statsmodels, models with explanatory variables are in the form of “regression with SARIMA errors”.statsmodelsalso supports vector moving-average (VMA) models using the same model class as described here for the VAR case, but, for brevity, we do not explicitly discuss them here.A second class,

VAR, can also be used to fit VAR models, using least squares. However, it lacks some of the features relevant for Bayesian inference discussed in this paper.Statsmodelscurrently contains two implementations of simulation smoothers for the linear Gaussian state space model. The default is the “mean correction” simulation smoother of Durbin & Koopman (2002). The precision-based simulation smoother of Chan & Jeliazkov (2009) can alternatively be used by specifyingmethod='cfa'when creating the simulation smoother object.While a detailed description of these issues is out of the scope of this paper, there are many superb references on this topic. We refer the interested reader to West & Harrison (1999), which provides a book-length treatment of Bayesian inference for state space models, and Kim & Nelson (1999), which provides many examples and applications.

This model is often referred to as a “local linear trend” model (with additionally a seasonal component);

lltrendis an abbreviation of this name.The popular Prophet library, Taylor & Letham (2017), similarly uses an additive model combined with Bayesian sampling methods to produce forecasts and decompositions, although its underlying model is a GAM rather than a state space model.

In this example, we used a local linear trend model with no seasonal component.

See, for example, Stock & Watson (2016) for an application of these techniques that handles outliers, Kim et al. (1998) for stochastic volatility, and Kim & Nelson (1998) for an application to dynamic factor models with regime switching.

- ARMA

- autoregressive moving-average

- DFM

- dynamic factor model

- GAM

- generalized additive models

- GLM

- generalized linear models

- GS

- Gibbs sampling

- HMC

- Hamiltonian Monte Carlo

- MCMC

- Markov chain Monte Carlo

- MH

- Metropolis-Hastings

- MLE

- maximum likelihood estimation

- NUTS

- no-U-turn sampling

- SSM

- state space model

- VAR

- vector autoregressive

- VMA

- vector moving-average

- Seabold, S., & Perktold, J. (2010). Statsmodels: Econometric and Statistical Modeling with Python. In S. van der Walt & J. Millman (Eds.), Proceedings of the 9th Python in Science Conference (pp. 92–96). 10.25080/Majora-92bf1922-011

- McKinney, W., Perktold, J., & Seabold, S. (2011). Time Series Analysis in Python with statsmodels. In S. van der Walt & J. Millman (Eds.), Proceedings of the 10th Python in Science Conference (pp. 107–113). 10.25080/Majora-ebaa42b7-012

- Salvatier, J., Wiecki, T. V., & Fonnesbeck, C. (2016). Probabilistic programming in Python using PyMC3. PeerJ Computer Science, 2, e55. 10.7717/peerj-cs.55

- Carpenter, B., Gelman, A., Hoffman, M. D., Lee, D., Goodrich, B., Betancourt, M., Brubaker, M., Guo, J., Li, P., & Riddell, A. (2017). Stan : A Probabilistic Programming Language. Journal of Statistical Software, 76(1). 10.18637/jss.v076.i01

- Dillon, J. V., Langmore, I., Tran, D., Brevdo, E., Vasudevan, S., Moore, D., Patton, B., Alemi, A., Hoffman, M., & Saurous, R. A. (2017). TensorFlow Distributions (Techreport arXiv:1711.10604). arXiv. 10.48550/arXiv.1711.10604

- Kumar, R., Carroll, C., Hartikainen, A., & Martin, O. (2019). ArviZ a unified library for exploratory analysis of Bayesian models in Python. Journal of Open Source Software, 4(33), 1143. 10.21105/joss.01143

- Hyndman, R., Koehler, A. B., Ord, J. K., & Snyder, R. D. (2008). Forecasting with Exponential Smoothing: The State Space Approach. Springer Science & Business Media.

- Hyndman, R. J., & Athanasopoulos, G. (2018). Forecasting: principles and practice. OTexts.

- Harvey, A. C. (1990). Forecasting, Structural Time Series Models and the Kalman Filter. Cambridge University Press.

- Brodersen, K. H., Gallusser, F., Koehler, J., Remy, N., & Scott, S. L. (2015). Inferring causal impact using Bayesian structural time-series models. Annals of Applied Statistics, 9, 247–274. 10.1214/14-aoas788

- Taylor, S. J., & Letham, B. (2017). Forecasting at scale (Techreport e3190v2). PeerJ Inc. 10.7287/peerj.preprints.3190v2

- Durbin, J., & Koopman, S. J. (2012). Time Series Analysis by State Space Methods: Second Edition. Oxford University Press.

- Fulton, C. (2015). Estimating time series models by state space methods in python: Statsmodels.

- Durbin, J., & Koopman, S. J. (2002). A simple and efficient simulation smoother for state space time series analysis. Biometrika, 89(3), 603–616. 10.1093/biomet/89.3.603

- Chan, J. C. C., & Jeliazkov, I. (2009). Efficient simulation and integrated likelihood estimation in state space models. International Journal of Mathematical Modelling and Numerical Optimisation, 1(1–2), 101–120. 10.1504/IJMMNO.2009.030090